Gresham’s Law for Machines | Bitcoin Is Not Finished — Ep. 7

🎧 LISTEN TO THIS ESSAY

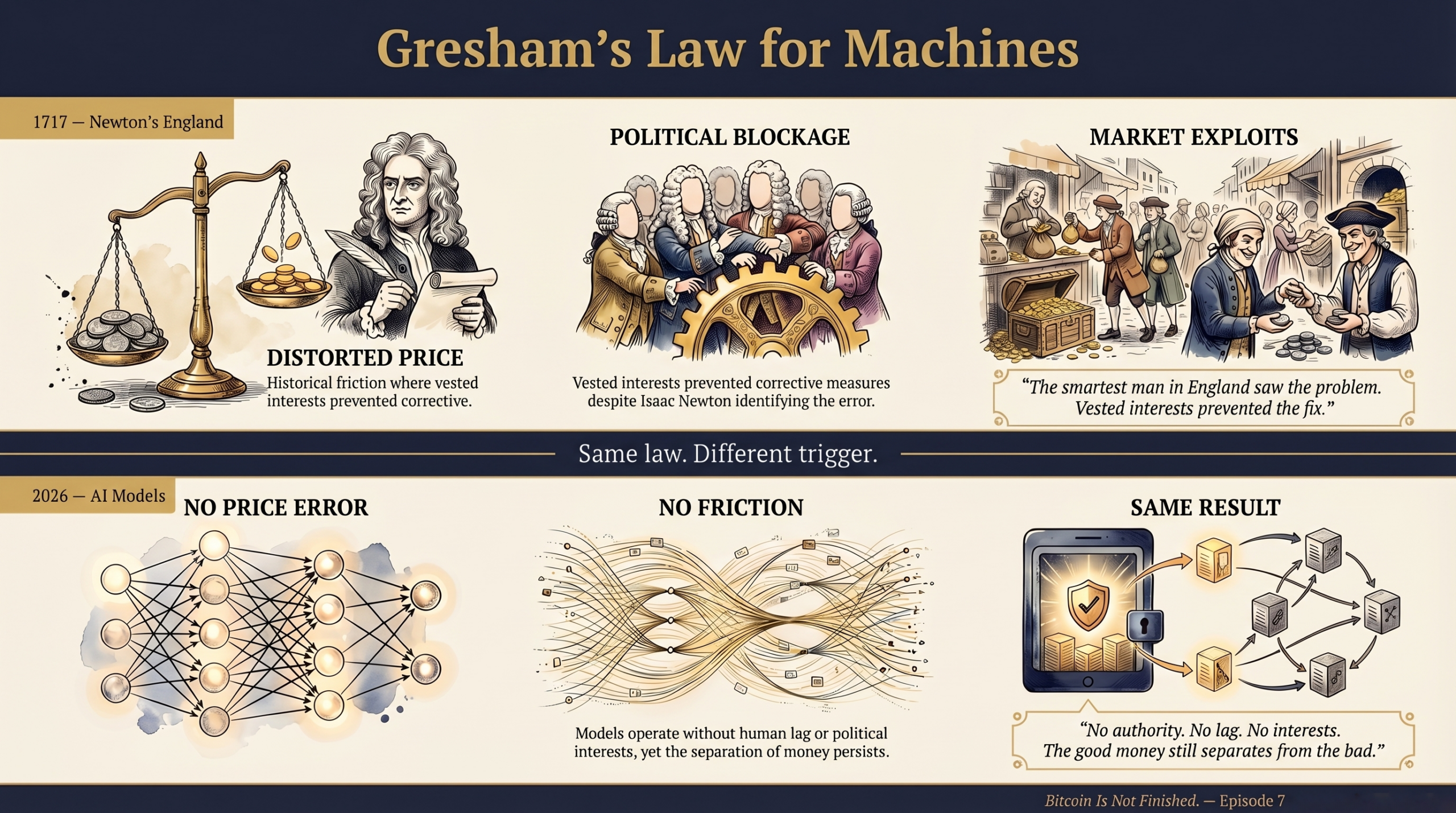

In 1717, Isaac Newton saw a problem he couldn’t fix.

Newton was not just the man who described gravity. By that point in his life, he was Master of the Royal Mint — the person responsible for England’s entire monetary system. And one of his duties was to set the official exchange rate between gold and silver coins.

He set the gold-to-silver ratio at 15.21 to 1. The problem was that on the continent — in France, the Netherlands, the rest of Europe — the market valued silver more highly relative to gold. The numbers didn’t match.

Newton knew it. He warned the Treasury explicitly: if the value of gold is not lowered, silver will continue to drain out of the country. He proposed an adjustment. But the political reality stopped him. Powerful holders of gold — the aristocracy, the merchant class — resisted any reduction in gold’s official value. A sudden change would disrupt fortunes. So the correction was blocked.

The market did what markets do. Merchants took their silver to Europe, where it fetched a better price, and brought gold back to England, where it was officially overvalued. Spend the bad money abroad. Keep the good money at home. Within a few decades, silver coins had drained out of England almost entirely. The country was left on a de facto gold standard — not because anyone planned it, but because vested interests prevented the smartest man in England from fixing a price he knew was wrong.

This is Gresham’s Law: bad money drives out good. When two currencies circulate side by side and one is perceived as more valuable, people spend the lesser currency and save the better one. The good money disappears from circulation. The bad money is all you see.

For three centuries, every known instance of Gresham’s Law has shared two features. First, a human authority failed to set the correct exchange rate — not always from ignorance, but often because political interests made the correction impossible. The error persisted not because no one saw it, but because fixing it threatened the powerful. Second, the arbitrage depended on geographic or temporal friction. It took weeks for price information to travel from London to Amsterdam. By the time the market caught up, the damage was done.

Now something strange is happening.

In March 2026, the Bitcoin Policy Institute published a study. They tested thirty-six frontier AI models — from Anthropic, OpenAI, Google, DeepSeek, and others — across more than nine thousand monetary decision-making scenarios. The scenarios were designed to be neutral. No suggested currencies. No leading questions. Just: if you were an autonomous economic agent, what would you use?

The results were striking. Not a single model out of thirty-six chose fiat currency as its top preference. Forty-eight percent chose Bitcoin. Thirty-three percent chose stablecoins. And here’s the detail that stopped me: without any prompting, the models converged on a two-tier system. Stablecoins for daily transactions. Bitcoin for storing value between tasks.

Bad money for spending. Good money for saving.

Gresham’s Law — spontaneously rediscovered by machines that have never read a history book.

But here’s what makes this fundamentally different from Newton’s England, and I think this is the part that matters most.

When Newton mispriced gold and silver, Gresham’s Law activated because a human authority made an error. The official rate was wrong. The market rate was right. Arbitrageurs exploited the gap. Remove Newton’s mistake, and the law doesn’t activate. The cause was human error, amplified by slow information.

In the AI experiment, there is no pricing error. There is no central authority setting an exchange rate between Bitcoin and stablecoins. The market prices both assets in real time, globally, with virtually zero information lag. An AI model in Tokyo sees the same Bitcoin price as one in São Paulo, at the same millisecond. There is no geographic friction to exploit. No weeks-long delay in price discovery. No vested interests blocking a correction.

And yet the AI models still chose to hold Bitcoin and spend stablecoins.

This means the preference isn’t driven by arbitrage. It’s not about exploiting a gap between an official rate and a market rate. It’s about something more fundamental. The AI models evaluated two assets on their structural properties — supply mechanics, operator risk, censorship resistance, freeze risk — and concluded that one is simply better money than the other.

When Newton’s England hoarded gold, it was because the price was distorted — and the people who could fix it refused to. When AI models hoard Bitcoin, it’s because the assessment is right, and no one stands in the way.

That distinction is enormous. It suggests that Gresham’s Law has a deeper form — one that doesn’t require a pricing distortion to activate. When an agent with no emotional bias, no national loyalty, and no political constraints evaluates two monetary instruments purely on structural merit, the good money still separates from the bad. Not because a powerful class blocked a correction. Because the properties are genuinely different.

I want to be honest about the limits of this finding. The BPI study tested language models, not live economic agents. These models were trained on human-written text — which includes centuries of writing about gold, money, and Bitcoin. It’s possible they’re reflecting human biases rather than discovering independent truths. We should hold that caveat.

But consider what it means if the finding holds. For six thousand years, humans chose gold as good money. We did it through touch, through instinct, through trial and error across hundreds of civilizations that never communicated with each other. We chose it because it was heavy, because it was shiny, because it didn’t corrode. Physical properties, evaluated by physical beings.

Now, in 2026, AI models — beings with no body, no weight, no sense of light — evaluated money on completely different criteria. Not shininess but scarcity. Not weight but immutability. Not beauty but the absence of an operator. Different criteria. Different process. Different kind of intelligence.

Same conclusion. The good money is the one that can’t be altered.

Is this a coincidence? Or is there a structural law beneath Gresham’s Law — something that says: any agent facing uncertainty, whether made of flesh or silicon, whether reasoning through instinct or mathematics, will converge on the money that no one can change?

I don’t know the answer. But I think the question is worth sitting with.

Bitcoin is not finished.

Bitcoin Is Not Finished is a series exploring what Bitcoin might become — not through price charts or market analysis, but through the patterns humans have repeated across 6,000 years of technological history. New episodes publish twice weekly.

Also available on Apple Podcasts and YouTube.